The first half of 2022 has passed quietly. Under the impact of multiple factors such as geopolitical conflicts, global hyperinflation, and demand overdraft, the global TV panel market has ushered in the darkest moment.

The end demand in the global TV market continues to be sluggish, brands are deeply controlling their inventory, the prices of LCD TV panels have fallen below the cash cost, and panel makers have also started the largest production cut in history. In 22H2, there are still relatively large uncertainties in the end market. The key to stabilize supply and demand in the global LCD TV panel market in 22H2 is whether the adjustment of panel maker capacity can catch up with the decline of the demand for brand panel purchasing.

{kind=link}

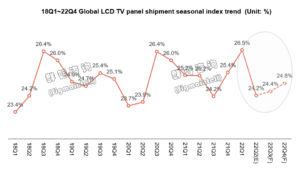

Panel Shipments: Seasonal Index Shows “L” Shape, Average Size Declines For The First Time

The seasonal index showed an “L” shape, and demand will remain weak in 22H2. The annual seasonal index of the global LCD TV panel market usually presents a “V”-shaped characteristic, but the seasonal index of panel shipments in 2022 appears to be an “L”-shaped. The peak season in 22H2 is not prosperous, and demand will still be weak.

• Q1: Affected by factors such as high inflation, high shipping costs, and demand overdraft in the end market, the retail performance was not as good as expected, and the demand for large-size panels of top brands was sluggish; Second-tier makers started the first round of bargain hunting and stocking, which drove the number of panel shipments in Q1 to a record high in Q1 and became the peak of the year.

• Q2: The Russian-Ukrainian war broke out, and the demand in the European market uncontrollably declined. Brand purchasing demand shrank to a new low in the past ten years than expected. Large-size demand continued to deteriorate, and small-size demand also declined. Panel shipments decreased rapidly in Q2.

• Q3: Samsung suspended panel purchases and is expected to continue its inventory control strategy in Q3. At the same time, pessimism spreads and affects the purchasing confidence of other brands, and panel shipments in Q3 may not be prosperous in the peak season.

• Q4: As shipping costs continue to fall, panel prices decline to a low level, and brand inventory tends to be healthy, it is expected that the stocking demand for top brand panels, especially large-size demand, is expected to resume growth in Q4, but there is no strong recovery in end consumption. It is difficult to expect a strong recovery in shipments.

According to Sigmaintell’s data, the global LCD TV panel shipment is expected to be 260 million in 2022, of which 68 million were shipped in Q1, accounting for 26.5% of the annual shipment; From Q2 to Q4, it is expected that the quarterly shipment level will fluctuate around 62 million pieces, and the seasonal index is difficult to exceed 25%, and the seasonal index has an obvious “L” shape.

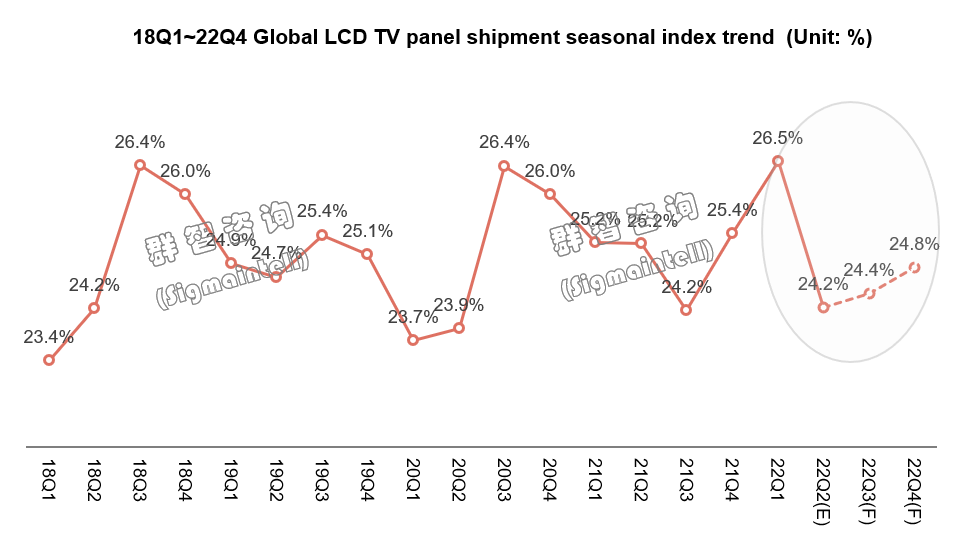

The large-scale size was hindered, and the average size and area decreased YOY. The upgrade and iteration of the generation line drive the process of large-size, which is the main trend of the development of the global TV panel market. However, the average size of the global LCD TV panel market will decline for the first time in 2022. The main reasons are as follows:

First, due to factors such as high inflation, high shipping costs, and demand overdrafts, the demand for large-size TVs in the North American market has been significantly suppressed;

Second, high inflation has brought about a global downgrade of consumption, hindering the process of large-scale size;

Third, panel prices drive makers to be more aggressive in stocking small sizes. The 32-inch panel with high price elasticity is the most typical, and the second-tier market demand, such as OEM/ODMs and distributors, occupies half of its shipments. When the price of the panel fell to a relatively low level, the enthusiasm of the second-tier makers was ignited, and the stocking behavior of the second-tier makers pushed up the 32-inch shipment level of the panel maker.

According to Sigmaintell’s data, the overall average size in 2022 is 47.7 inches, a decrease of 0.8 inches YOY. In the first three quarters, due to the sluggish demand for large sizes and the high level of 32-inch shipments, the average size is lower than that in 2021. It is expected that with the advent of the “11.11” promotion season in China, the inventory of brands and channels in the North American market tends to be healthy, and the logistics and panel costs will further decline. It is expected to drive the recovery of large-size demand, thereby promoting the global average size of LCD TV panels to increase to 49.3 inches in Q4, a significant increase of 2 inches from the previous quarter.

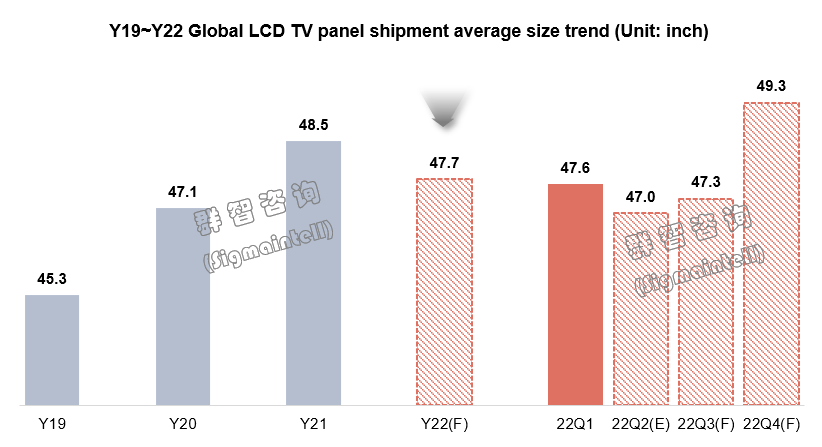

The OLED panel market is also difficult to survive alone, falling into the dual dilemma of loss expectations and shrinking volumes. In the background of high global inflation, especially the decline in demand in Europe and North America, the demand for OLED TV panels has been hit hard. First, high inflation has had a severe impact on the demand for entry-level OLED TVs. Secondly, the impact of the price difference of LCD panels has intensified, the price of OLED TV panels has remained high for a long time, and the profits of TV brands have been squeezed, which has led to more conservative strategies and further suppressed demand. Finally, Samsung Electronics suspended the launch of WOLED products in 2022, which has caused a heavy blow to LGD’s annual OLED TV panel shipments. Affected by the above factors, the shipment of WOLED panels in 2022 will be much lower than expected, with high inventories starting from the first quarter and gradually reducing the UT of the G8.5 OLED panel production line in South Korea from the second quarter. The reduction in the UT is accompanied by an increase in costs, and the WOLED panel business may fall into the dual dilemma of loss expectations and shrinking volumes. Overall, according to Sigmaintell’s data, with the support of SDC QD Display panels, the global OLED TV panel shipments in 2022 will be 8.88 million units, an increase of 15.0% YoY, which is lower than expected.

Panel maker strategy: Initiate the largest production cut in history

As LCD TV panel prices have fallen below cash costs; panel makers are under enormous pressure to lose money. It is difficult to expect the recovery of end demand in the short term, and panel makers have started the production cut, but each maker has different strategies.

BOE passively reduced production, mainly reducing the capacity of G10.5 and G8.6. Thanks to the advantages of balanced development of multiple categories, the profit of IT panels can still provide a certain guarantee for a high UT and stable operation to BOE. However, after global brands such as Samsung Electronics and LG Electronics made clear their strategy of continuing to control inventory in Q3, the demand situation was not optimistic, and passive production cuts were initiated. Among them, the UT of G8.6 and G10.5 lines has been lowered to a certain extent.

CSOT, the pace of production cut is steadily progressing, mainly reducing the supply of 65-inch and 75-inch panels. CSOT is very dependent on two major customers: Samsung and TCL. Samsung’s procurement strategy adjustment has put enormous pressure on CSOT, and it has reduced production since June. CSOT ‘s capacity adjustment is mainly focused on the supply of 65-inch and 75-inch panels.

HKC’s ramp-up slowed down, and production expansion was delayed. Affected by the decline in demand, HKC faces greater shipping resistance and inventory pressure. HKC has also gradually started capacity control since June, which is mainly reflected in the slowdown of the new H4 and H5 lines. It is expected that the UT will remain at a low level in Q3.

Taiwan’s panel makers have differentiated strategies and are oriented to operating profit. For Taiwan panel makers, once the price of LCD TV panels hits the red line of cost and drags down profit performance, they will accelerate the contraction of the TV business. AUO has adjusted its capacity since the beginning of Q2. As the demand for various applications continues to decline, the adjustment range of UT gradually spreads from G6 to G8.5. Innolux’s UT adjustment is relatively conservative, mainly reflected in the further control of the 50-inch supply and the transfer of TV capacity to IT, and the supply of TV panels continues to decline.

South Korean panel makers have withdrawn some capacity, and the competitiveness of LCD TV panels has weakened. The cost competitiveness of LCD TV panels of Korean makers is low. As panel prices fall uncontrollably, they will more resolutely implement production control. SDC has closed all of its LCD TV panel production lines and started to maintain inventory shipments in June; The LGD G7.5 line has been gradually reduced since May, and the capacity of Guangzhou’s G8.5 line has also been controlled.

Overall, as panel makers have started to cut production, it has had a certain adjustment effect on the global supply of LCD TV panels. According to Sigmaintell’s data, in Q2, the global LCD TV panel supply area decreased by 1.4% YoY and 2.9% MoM. It is expected that the global LCD TV panel supply area will further decline by 7.3% YoY in Q3. However, in Q3, panel demand fell into a deep destocking cycle, and the decline in panel procurement demand was still higher than the reduction in panel maker production. The global LCD TV panel supply and demand situation are still not optimistic.

Supply and demand and prices: Supply and demand continues to be in excess in Q3, and prices maintaine a downward trend

In Q3, the two major South Korean brands still strictly controlled their inventory, so the purchasing strategies of Chinese brands also fell into conservative expectations. According to Sigmaintell’s data, the global top 9 TV panel brand purchase demand is expected to be less than 35 million units in Q3, the lowest level in the past five years. On the supply side, although top panel makers have initiated passive production cuts, the reduction in capacity still cannot keep up with the decline in demand. According to Sigmaintell’s data, the global LCD TV panel market S/D ratio will reach 8.6% in Q3, and the supply and demand will continue to be in excess. It is expected that panel prices will maintain a downward trend at a low level.

Out of the dilemma: actively promote cost reduction and efficiency increase, and need to increase the scale of production cut in the short term

The price of LCD TV panels continues to decline, while the prices of other types of panels also show an accelerated downward trend. So the pressure on panel makers to lose money increased sharply. However, the global economic and political environment is still unstable, and high inflation may not be effectively alleviated in the short term. Therefore, it is difficult to expect a strong recovery in the global TV market demand. At this dark moment, how can TV panel makers get out of the dilemma? When will supply and demand return to balance? When will panel prices stop declining? Sigmaintell believes that in the short term, it is necessary to increase the scale of production cut. At the same time, since cost is the core competitiveness, cost reduction and efficiency improvement should be actively promoted.